The December oil rush

When Gullfaks began production in December 1986 instead of January 1987, Statoil was able to start its tax depreciation one year earlier than it otherwise would have. Whether Statoil deliberately accelerated production at Gullfaks to save on taxes is uncertain. However, across the Norwegian continental shelf, a striking number of fields started production in December in the years leading up to 1987.

To understand why Statoil could benefit from bringing production forward by a calendar year, it helps to understand how tax depreciation works.

Corporate tax, which all companies (including oil companies) must pay, provides a useful example. Norway taxes corporate profits through corporate income tax. If a company invests NOK 100 and earns NOK 150, the profit is NOK 50. Tax is paid on this profit, calculated as a percentage of both revenue and costs.

In 2024, Norway’s corporate tax rate is 22 percent. In our example, this means the state:

- Collects 22 percent of the NOK 150 in revenue (NOK 33)

- Covers 22 percent of the NOK 100 in costs (NOK 22)

In total, the company effectively pays NOK 33 – 22 = NOK 11 in corporate tax (which is 22 percent of the NOK 50 profit).

Why companies want faster depreciation

“Depreciation” refers to the portion of costs deducted from taxable income—the part the state reimburses. The key question is when and how this reimbursement occurs.

Under the standard corporate tax regime, the state’s share of investment costs (depreciation) is refunded only after the company starts making a profit. Depreciation occurs gradually over six years, starting when production begins.

In addition to corporate tax, oil companies have been subject to a special petroleum tax since 1975. In total, oil companies pay 78 percent tax on their profits. Until 1987, the special tax was structured so that depreciation could only begin after a field started production.

Naturally, companies prefer to depreciate costs as quickly as possible. A krone today is worth more than a krone tomorrow. If companies receive the state’s share of costs immediately when making an investment, they can reinvest the money elsewhere—whether in new offshore projects or interest-bearing savings.

This impatience is particularly pronounced in the oil industry, where investments tie up large amounts of capital in a highly uncertain market. As a result, oil companies demand high returns before committing to investments.

In 2018, oil companies’ annual required rate of return was estimated at 13–14 percent[REMOVE]Fotnote: Fotnote: Finansdepartementet. (2018). Klimarisiko og norsk økonomi: Bakgrunnsnotat om petroleumssektoren (NOU 2018:17). https://www.regjeringen.no/no/dokumenter/nou-2018-17/id2622043/?q=avkastningskrav&ch=4#match_0 This means they would require NOK 1.14 next year for every NOK 1 invested today. That is higher than in many other industries. We do not know the exact return requirements Statoil or other oil companies had in 1986 or have today, but we do know they have historically been quite high.

By bringing production forward from 1987 to 1986, Statoil was able to accelerate depreciation and avoid tying up capital longer than necessary. While tax savings alone do not prove that the decision to accelerate production was tax-driven, the tax system likely played a role.

The December effect: strategic timing or coincidence?

To assess whether December start-ups were tax-motivated, we can compare production start dates before and after 1987. At the end of 1987, Norway’s tax regime changed, allowing companies to begin depreciation on the special petroleum tax as soon as investments were made, rather than waiting until production began.[REMOVE]Fotnote: Ot. Prp. Nr. 3 (1986 – 1987) Om lov om endring i lov av 13. Juni 1975 om skattlegging av undersjøiske petroleumsforekomster m.v This change reduced the financial incentive to bring production forward to the end of the calendar year.

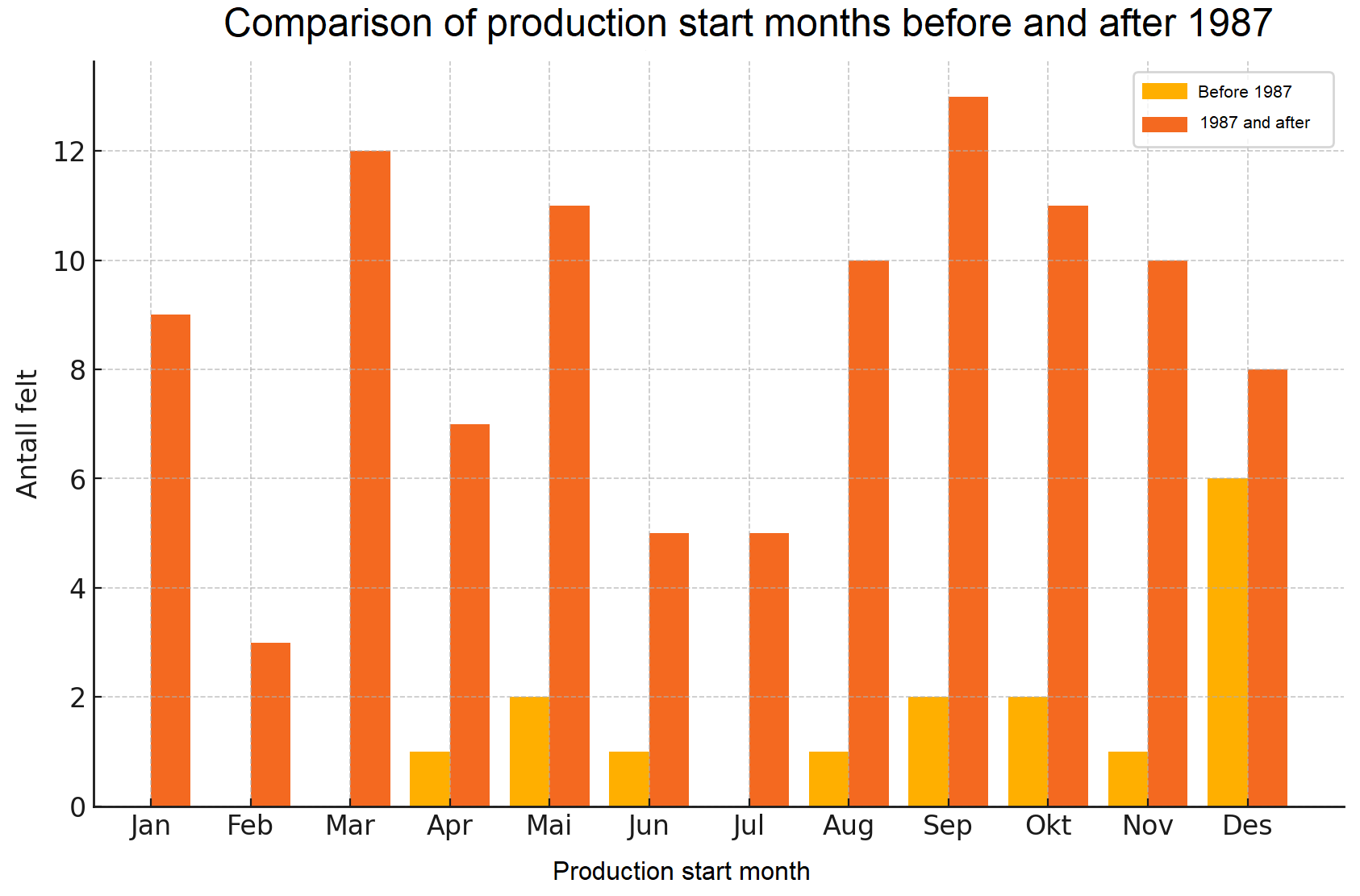

The figure below shows the distribution of production start months for all fields on the Norwegian continental shelf, both before and after 1987. It demonstrates a clear (and statistically significant) overrepresentation of “December-born” fields before 1987, an effect that disappears for fields brought into production after the tax change.[REMOVE]Fotnote: The overrepresentation in December is statistically significant, with a 99% confidence interval. 36% of the fields started production in December. If start dates were completely random (the null hypothesis), the expected share would be one-twelfth (8.3%). The standard deviation for the percentage of fields starting per month is 0.108. The probability of the observed number of December start-ups up to 1987 is given by P(Z), where Z = ((0.36 – 0.083) / 0.108). This results in P(Z = 2.62), which is less than 0.001. Thus, we can conclude that certain factors made it more likely for fields before 1987 to start production in December than in other months.

This suggests that companies deliberately timed production start-ups to occur before year-end, where possible.

Caution: tax incentives were not necessarily the decisive factor

Until 1987, no oil fields began production in the first three months of the year, while 36 percent started in December. After 1987, production start dates were more evenly distributed throughout the year. It is reasonable to assume that tax system changes influenced this shift. However, other factors may also have played a role.

A likely explanation is that offshore platform installations typically occur in favorable weather conditions, usually in the summer months. Since it takes time to prepare a platform for production, fewer start-ups are expected in these months.

Differences between the pre- and post-1987 periods could also be due to changes in platform technology. Newer installation types may require less preparation time or be easier to transport to offshore locations under difficult weather conditions.

If this is the case, it suggests a broader trend on the Norwegian continental shelf, with start dates becoming more evenly distributed over time, regardless of tax rules.

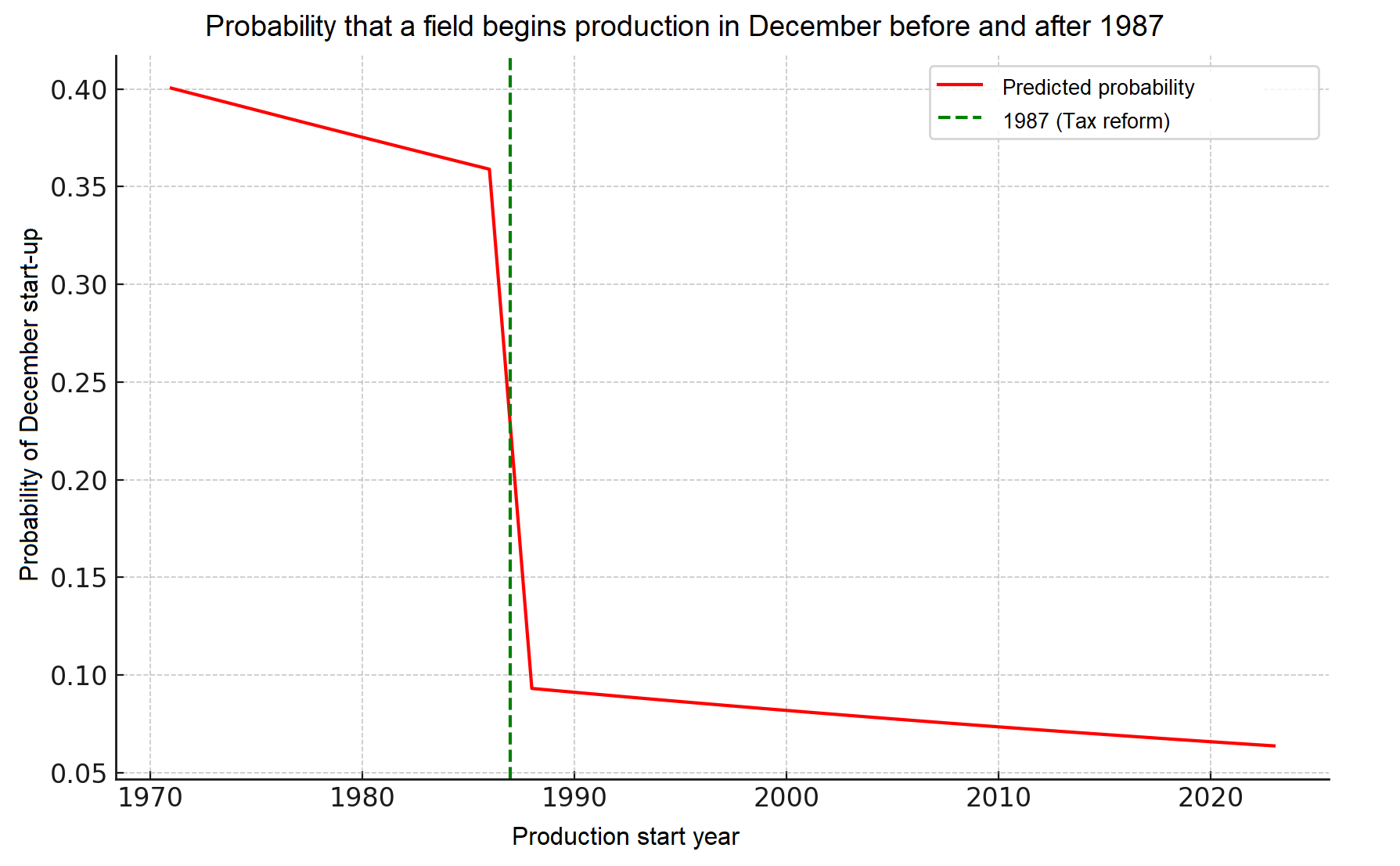

The figure below shows the probability of a field beginning production in December over time. It captures both the drop in December start-ups after 1987 and the broader trend of more evenly distributed start dates.[REMOVE]Fotnote: To separate the general trend from the jump in a specific year (1987), a Regression Discontinuity Design (RDD) approach was used .The model is logistic and estimates the probability of a field starting production in December. This approach allows for distinguishing the overall trend from the discontinuity that occurs in the specified year

As expected, the probability of December start-ups declines in 1987. However, after controlling for the general trend, the drop is no longer statistically significant.[REMOVE]Fotnote: A Regression Discontinuity Design (RDD) analysis was conducted using a logistic regression model to assess changes in the probability of a field starting production in December. The results show that the probability of December start-ups declines in 1987, but this change is not statistically significant. The likelihood that the observed jump (the discontinuity in the regression model) is due to random variation is 13.5% (p = 0.135). This suggests that while there is a tendency for fewer December start-ups after 1987, the change is not strong enough to be statistically confirmed.

There is a 13.5 percent probability that the decline in December start-ups was due to random variation rather than a specific tax-related event.

This may seem surprising, given the sharp drop in December start-ups from 36 percent in 1986 to 9 percent in 1987. However, the sample size before 1988 was small (16 fields), and the December overrepresentation was not large enough to definitively rule out other explanations.

Economic inefficiency caused by tax-driven decisions

Even if the tax system was only one of several factors, it is likely that some of the December start-ups before 1987 were influenced by depreciation rules. From a broader economic perspective, this is problematic.

Bringing production forward has clear advantages—mainly that revenue starts flowing earlier. However, it also comes with costs. These may include overuse of labor and capital, compressed development timelines leading to seasonal fluctuations, or even compromises on safety procedures.

In a well-functioning market, companies balance these costs and benefits optimally. However, when the tax system creates artificial incentives to accelerate production, it distorts decision-making. Unlike the real costs and benefits mentioned above, the tax incentive does not reflect actual economic factors. Instead, it arbitrarily encourages earlier production start-ups, potentially leading to inefficient resource use.