Petoro is more than a tax

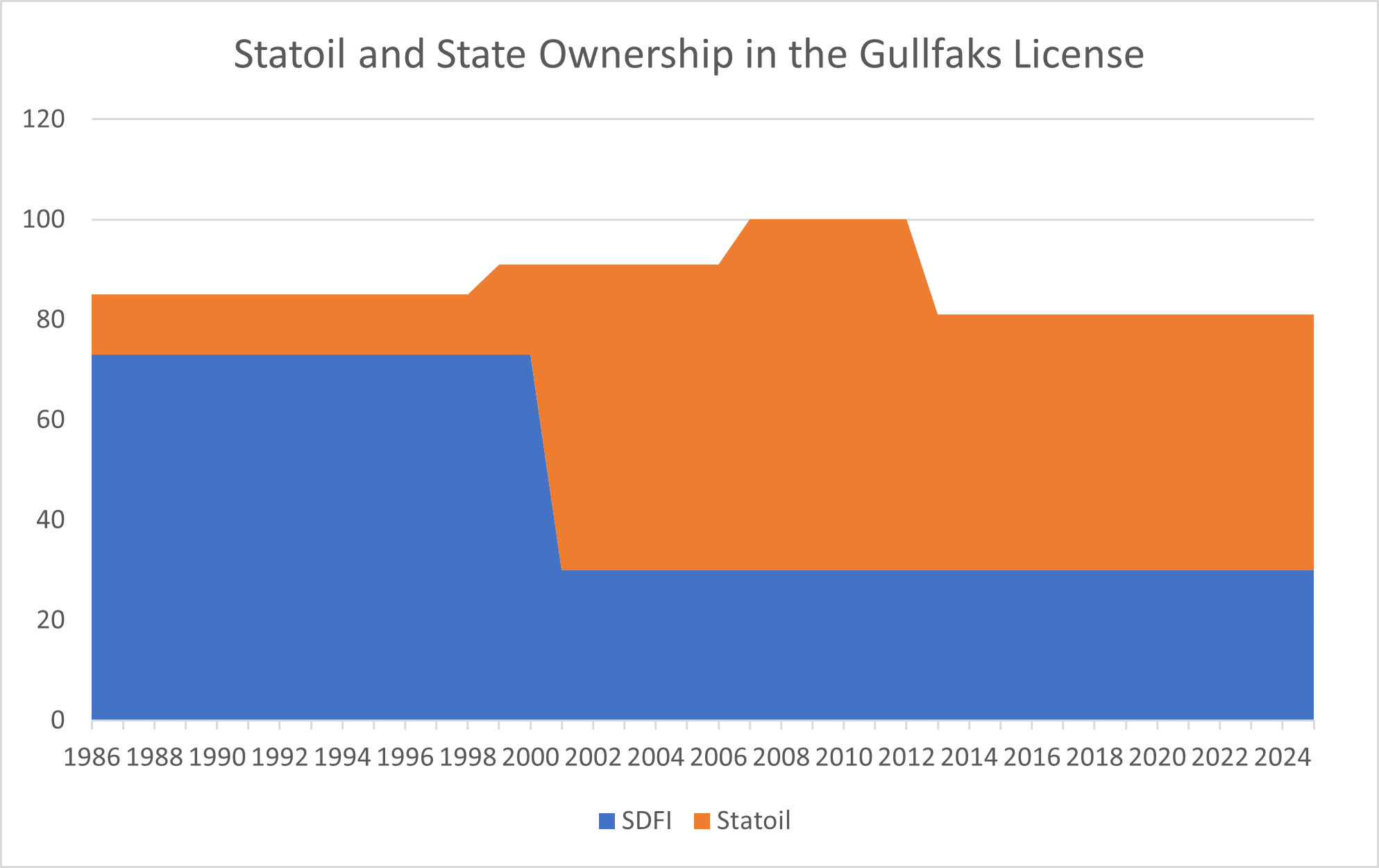

This article examines the main characteristics of Gullfaks’s largest historical owner: the state, through the State’s Direct Financial Interest (SDFI).[REMOVE]Fotnote: If we add up the ownership shares in Gullfaks year by year over the lifetime of the field, Statoil has held an ownership share equivalent to 16.2 years at 100 percent ownership. The state, through the State’s Direct Financial Interest (SDFI), has held an equivalent of 17.4 years. The calculation covers the period from January 1, 1987 to December 31, 2025.

What impact has that ownership had — or might it have had — on the development of the field?

It also looks at how Petoro, which today manages the SDFI, differs from a traditional oil company. While it is difficult to determine exactly how the high SDFI share (73% between 1985 and 2001) may have influenced day-to-day operations at Gullfaks, we can say a lot about what kind of owner Petoro is, and how state ownership shapes the Norwegian Continental Shelf more broadly.

What is the SDFI?

Ask a Ministry of Finance official to define the State’s Direct Financial Interest (SDFI) and explain what Petoro — the company that manages it — actually is, and you might hear the following: Petoro and the SDFI are like a tax.

That’s obviously an oversimplification — but there’s a fair amount of truth in it.

The SDFI was created at the beginning of 1985. The reform meant that the state became a direct equity holder in several licenses, paying its share of investments and operating costs — and receiving a corresponding share of the revenues. That structure is strikingly similar to the special petroleum tax on oil companies’ profits as applied by the Norwegian authorities.[REMOVE]Fotnote:In 2025, the Norwegian state applies a cash flow tax system, meaning it collects a share of oil companies’ profits — both revenues and costs.

See: Norwegian Ministry of Finance. (2021, September 3). Consultation paper – Reform of the special petroleum tax into a cash flow tax. Government of Norway. https://www.regjeringen.no/contentassets/02a51e6558b24780beafab886fa9523b/horingsnotat.pdf

Between 1985 and 2001, the SDFI shares were managed by Statoil, which was required to maximize the total return from both its own and the state’s license holdings. After Statoil was partially privatized, responsibility for managing the SDFI was transferred to a wholly state-owned company: Petoro. This ensured continued national control and ownership of the shares.

Petoro holds license interests that together account for about 25 percent of all production on the Norwegian Continental Shelf. However, it is not an operating oil company. The company has just over 70 employees and a 2025 operating budget of NOK 400 million — a modest sum by oil industry standards. Even so, Petoro holds voting rights in the licenses and can, in principle, pursue its own agenda and argue for specific outcomes.

More than a tax mechanism

Petoro receives its funding via the national budget and transfers all profits back to the state. In other words, the state collects its SDFI revenues not through taxation but through the return of Petoro’s profits. Petoro itself is exempt from tax.

This exemption has an important consequence: Unlike commercial, tax-paying companies that may be swayed by tax incentives, Petoro makes decisions without regard to tax optimization.

The petroleum tax regime in Norway is largely designed to avoid distorting investment decisions. In theory, any project that is profitable before tax should also be profitable after tax — and vice versa. But in practice, tax rules often create subtle incentives. Petoro, by contrast, can help steer decisions in licenses toward those that are truly profitable — before tax is considered.

There is also an argument that Petoro is less vulnerable to empire-building or brand management ambitions. As of 2024, Petoro is politically barred from expanding into other parts of the energy value chain. Its overarching mission is simple: to maximize revenues for the state.[REMOVE]Fotnote: Olje- og energidepartementet. (2002, 1. oktober). Hovedinstruks for økonomiforvaltningen av SDØE i Petoro. https://www.regjeringen.no/globalassets/upload/oed/vedlegg/statlig-engasjement/petoro_1_okonomiinstruks.pdfThat makes it harder for the company to support costly or unprofitable projects driven by political rather than economic motives.[REMOVE]Fotnote: Hovland, K. M. (2023, 26. november). Frykter at Petoro bremser havvind på sokkelen. E24. https://e24.no/energi-og-klima/i/dwA0rq/frykter-at-petoro-bremser-havvind-paa-sokkelen If Petoro were to spend on unprofitable projects, it would effectively be a form of hidden oil fund spending — and fall outside the limits set by the fiscal rule.[REMOVE]Fotnote: Kvadsheim, O. (2023, 19. desember). Ikke lurt å gjøre Petoro til et politisk verktøy. Stavanger Aftenblad. https://www.aftenbladet.no/meninger/kommentar/i/69EBl0/ikke-lurt-aa-gjoere-petoro-til-et-politisk-verktoey In spring 2024, representatives from the Conservative and Liberal parties proposed giving Petoro broader authority to invest in offshore wind. When the motion was rejected, the Minister of Energy explained that such a change would reduce transparency and control over Norway’s use of oil revenues.[REMOVE]Fotnote: Stortinget. (2024). Representantforslag om krav til erstatningskraft for elektrifisering av petroleumsinstallasjoner (Dokument 8:118 S (2023–2024), Innst. 394 S (2023–2024)). Hentet fra https://www.stortinget.no/no/Saker-og-publikasjoner/Saker/Sak/?p=98202

A built-in life support system?

Petoro’s annual letter of assignment from the state often highlights a key priority: the company should use its influence in licenses to help realize reserves and increase recovery from mature fields. In other words, Petoro is expected to play a central role in extending the lifespan of aging infrastructure.

This goal is somewhat counterintuitive.

From an economic standpoint, there are strong arguments for the state to do the opposite in the case of large fields with high decommissioning costs that are deep into their tail-end production phase.[REMOVE]Fotnote: Hoel, M. (2018). Avslutning av oljefelt (Rapport nr. 2018/36). Vista Analyse. https://www.vista-analyse.no/en/publications/avslutning-av-oljefelt/

The reason lies in differing return requirements. Each actor — whether government or private company — has a threshold for what rate of return is considered acceptable when evaluating an investment. These required returns are business secrets, but a 2018 estimate suggested that oil companies at the time generally required a return of 13–14 percent.[REMOVE]Fotnote: NOU 2018: 17. Klimarisiko og norsk økonomi (Kapittel 8.4.2). Regjeringen. https://www.regjeringen.no/no/dokumenter/nou-2018-17/id2622043/?ch=8

The state, by contrast, uses a 7 percent rate of return for offshore investments — substantially lower.

Any rate of return above zero implies that a krone is worth more today than tomorrow. Companies therefore have a built-in incentive to postpone costs when possible. The higher the required return, the stronger the preference to delay — and decommissioning is a major cost that companies often want to push into the future.

A 2018 report commissioned by the Norwegian Petroleum Directorate and authored by economist Michael Hoel showed that oil companies, when faced with high decommissioning costs and high return requirements, have a tendency to extend field lifetimes beyond what would be optimal from the state’s point of view.[REMOVE]Fotnote: Hoel, M. (2018). Avslutning av oljefelt (Rapport nr. 2018/36). Vista Analyse. https://www.vista-analyse.no/en/publications/avslutning-av-oljefelt/

While Petoro is not the state itself, it is fully state-owned. Still, it is not required to apply the same return assumptions used by the government. That makes sense: if other companies in a license knew Petoro was working with a lower threshold for profitability, they would likely take its input less seriously.

What’s notable is that the state has tasked Petoro with advocating for extended field life and increased recovery — even in cases where the state might ultimately benefit more from winding down production earlier.

A special relationship with Equinor?

Petoro is not an operator and does not market or sell its own oil and gas. This task is delegated to Equinor, which, under the marketing and sale instructions, is obligated to handle both its own and the state’s petroleum. Petoro’s role is to ensure that this is done properly and that revenues and costs are fairly allocated.

But Petoro’s objectives differ from those of other oil companies. According to its articles of association:

«Due to the state’s combined ownership strategy — as majority shareholder in Equinor ASA and owner of the state’s direct participating interests — the company shall consider the state’s overall ownership interests when making decisions that affect the implementation of the marketing arrangement.»[REMOVE]Fotnote: Petoro’s Articles of Association as of November 2024, § 11 Marketing of Petroleum, third paragraph:

This means that Petoro is expected to weigh both its own and Equinor’s profitability when it plays a role in petroleum sales — in order to maximize the state’s total return. Petoro is thus the only company on the Norwegian Continental Shelf that is explicitly tasked with considering the profitability of another company.

Given that this provision has been in place for many years, it is probably on solid legal ground, and unlikely to violate EEA competition or state aid rules. Still, the fact that a fully state-owned company can be instructed to — in principle — favor a partly state-owned commercial enterprise does highlight the kind of “wiggle room” Norway has within the EEA framework.

Information asymmetry

One final way Petoro differs from ordinary oil companies is in how difficult it is to estimate its economic value — both as a company and in terms of its individual license shares.

A commercial oil company typically has the administrative apparatus to assess the value of its own portfolio, and is subject to regular market valuation via the stock exchange. In contrast, Petoro’s share value is fixed at NOK 1,000 per share.[REMOVE]

Fotnote: Petoro’s Articles of Association as of November 2024, § 4 Share CapitalBut if we used the most recent market valuation estimate of Petoro’s license interests, a single share would be worth 158 times that amount.[REMOVE]Fotnote: Petoro. (2022). Årsrapport 2022 (s. 27). Petoro. Hentet fra https://www.petoro.no/%C3%85rsrapport-sider/2022/pdf/PetoroAarsrapport2022.pdf

If only it were possible, the Petroleum Museum’s top investment tip would be: buy Petoro shares — they’re undervalued!

But of course, Petoro shares are not for sale. Nor are its license shares actively traded. One reason is that it’s difficult to assess whether a proposed sale price is actually fair — making such transactions rare. As a result, Petoro behaves as a long-term investor in the licenses where it holds equity.

Summary

You’re not wrong to think of Petoro and the SDFI as resembling a kind of tax. The main role of Petoro is to hold license interests and transfer profits to the state — in a way that closely mirrors how the cash flow tax works in the petroleum sector.

But Petoro is more than that. It has voting rights and the ability to propose measures in the licenses it participates in — and it uses that power. Across the Norwegian Continental Shelf, Petoro’s presence tends to result in:

- Stricter profitability discipline and more cautious decision-making

- Extended recovery efforts in late-life fields

- Petroleum marketing strategies that benefit the state (or Equinor)

- Less license share trading and a more stable ownership presence

Implications for Gullfaks

It is difficult to pinpoint exactly how the SDFI has shaped the management of the Gullfaks field — largely because partners in a license are typically aligned, at least publicly. The points above, however, offer a basis for an informed guess about how the state’s ownership may have influenced the course of the field’s development.