Caught in the middle: How government tax cuts made Gullfaks less profitable

From November 1985 to July 1986, oil prices plummeted from $29.8 per barrel to $9.5 per barrel, severely impacting investment appetite in the industry. To maintain activity levels, the Brundtland government presented a proposal to Parliament on August 22, 1986, suggesting significant changes to the tax system for oil companies.[REMOVE]Fotnote: Stortinget. (1986-1987). Ot. Prp. Nr. 3. Om lov om endring i lov av 13. juni 1975 om skattlegging av undersjøiske petroleumsforekomster m.v.The goal of the tax package was to stimulate continued high activity levels on the continental shelf despite the sharp drop in oil prices.

To maintain activity levels, the government needed to ensure profitability in new projects.

The key tax measures in the proposal were:

- The removal of the production fee for new fields.

- Companies could begin depreciation on the special tax in the same year investments were made.

- The uplift allowance (where a portion of profits was shielded from the special tax) was replaced with a “production allowance.”

- The special tax rate was reduced from 35 to 30 percent.

Profitability in existing or already approved fields was less of a priority. This is because offshore installations are expensive to build but relatively cheap to operate. In other words, oil prices would have to be extremely low for a company to want to stop production from a fully developed field.[REMOVE]

Fotnote: Stortinget. (1986-1987). St. Meld. Nr. 41. Om enkelte spørsmål i petroleumsbeskatningen, s. 8.Since activity related to completed and ongoing fields was far less sensitive to changes in oil prices and tax regulations, these fields were not prioritized in the government’s tax package.

Fields caught in the middle

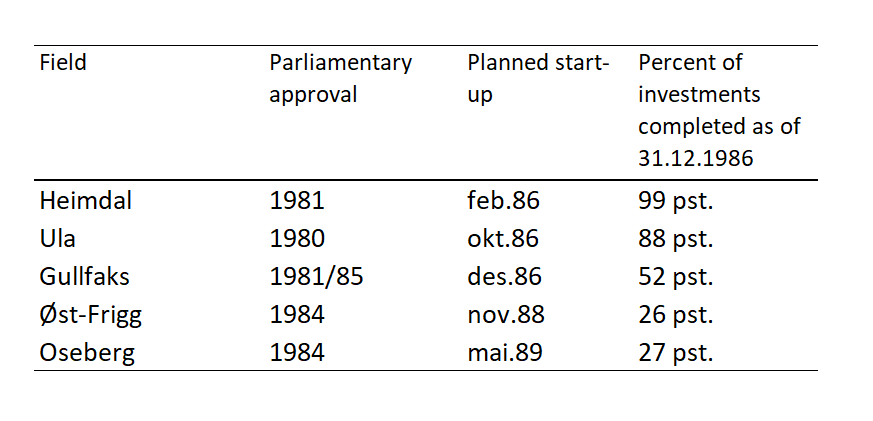

The tax changes made it more profitable for companies to develop new fields, while having little impact on fully developed ones. However, some fields, including Gullfaks, had been approved for development between 1981 and 1984, with production starting (or expected to start) between 1986 and 1989. For these fields, the impact of the tax changes was more uncertain. They could either become more or less profitable depending on how oil prices developed.

The Ministry of Finance identified five fields that could potentially lose out in the transition from one tax system to another: Gullfaks, Oseberg, East Frigg, Heimdal, and Ula. The companies had begun investing in these fields under the old tax regime, while production would take place under the new regime. The Ministry labeled them “transition fields.”

Impact of Uplift Loss and Reduced Special Tax

Gullfaks, along with the other transition fields, was affected by the tax changes in two ways: one change increased taxes, while the other reduced them.

On the one hand, Gullfaks lost its uplift allowance, leading to a higher tax burden. The uplift scheme allowed companies to shield a portion of their profits from the special tax. The amount of uplift a company received was based on its investment costs. The company was entitled to 6.6 percent of its investment costs as uplift. If a company had invested 100 million NOK in developing a field, 6.6 million NOK of its profits would be exempt from the special tax. Losing this uplift meant paying more in taxes.

On the other hand, the second tax change lowered the special tax rate from 35 percent to 30 percent. The special tax, which was in addition to the regular corporate tax, meant that a portion of the company’s profits went directly to the state. The new lower rate allowed companies to keep a larger share of their profits.

Which tax change had the strongest effect?

The impact of these two changes on the tax burden depended on how high oil prices became. Uplift was determined solely by how much a company had invested, not by sales revenue or oil prices. If a company invested 100 million NOK, it would receive 6.6 million NOK in uplift, regardless of whether it sold oil for 150 or 200 million NOK.

However, the amount of special tax paid increased with higher profits. Higher oil prices led to higher profits, which in turn resulted in higher special taxes. The reduced tax rate from 35 to 30 percent would result in significant savings for companies if oil prices and profits were high. On the other hand, if oil prices remained low, profits would be smaller, making the reduced tax rate less impactful. In essence, the amount companies saved from the lower special tax depended on oil prices. If oil prices were high enough, the positive effect of the lower special tax rate would outweigh the negative effect of losing the uplift allowance, from the companies’ perspective.

Whether the transition fields would ultimately lose out due to the tax changes depended on how oil prices developed in the coming years. Forecasts for future oil prices suggested that the transition fields would become less profitable overall due to the tax changes.[REMOVE]

Fotnote: Stortinget. (1986-1987). St. Meld. Nr. 41. Om enkelte spørsmål i petroleumsbeskatningen, s. 5

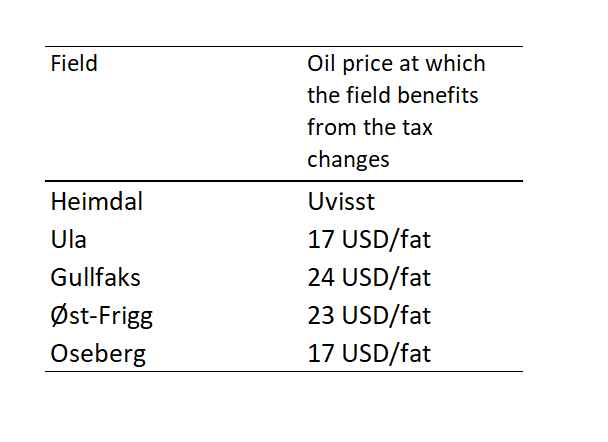

For Gullfaks to reach this milestone, the oil price needed to be at least $24 per barrel. In comparison, the Ministry of Finance’s oil price estimates ranged between $15 and $20 per barrel, which aligned fairly well with the actual prices throughout the 1990s. The oil price averaged well below $24 per barrel during much of the peak production period at Gullfaks. Therefore, it can be concluded that, from the oil companies’ perspective, Gullfaks became less profitable due to the tax changes. However, this is not to say that the field became unprofitable.

The Ministry of Finance acknowledged as early as 1986 that the loss of uplift on investments made after January 1. 1987, would not be compensated by the reduction in the special tax rate.[REMOVE]Fotnote: Stortinget. (1986-1987). St. Meld. Nr. 41. Om enkelte spørsmål i petroleumsbeskatningen, s. 5

The Finance Committee in the Norwegian Parliament feared that the tax measures could harm Norway’s reputation as a stable and predictable player, potentially deterring foreign companies and hindering competition and access to capital on the Norwegian continental shelf. In the long run, this could reduce Norway’s revenues from the shelf.

In response to these concerns, the Ministry of Finance pointed out that, overall, oil companies would benefit from the new tax regime. The fact that certain fields became less profitable from a business perspective was of lesser importance, as long as the companies were profitable overall.

The Ministry also highlighted the strong interest in exploration and development on the Norwegian continental shelf in recent years, indicating that the government’s policies were perceived as credible. In short, there was little to suggest that oil companies feared sudden, unexpected tax shocks.[REMOVE]Fotnote: Stortinget. (1986-1987). St. Meld. Nr. 41. Om enkelte spørsmål i petroleumsbeskatningen, s. 10-11

New fields became more profitable

Beyond the removal of the uplift allowance and the reduction in the special tax rate, the tax package included several changes that improved the profitability of new fields (from the oil companies’ perspective).

The most significant change was the removal of the production fee for new fields. Unlike the special tax, the production fee was a tax on revenues—not profits. Until 1987, 8–16 percent of a company’s sales revenue went directly to the state, regardless of the field’s profitability. This fee was now eliminated.

New fields were also given a new tax exemption scheme, which replaced the old uplift system: the production allowance. The production allowance meant that 15 percent of the total production value was deducted (shielded) when calculating the basis for the special tax.

The scheme was strikingly similar to the uplift system but with one key difference: where the uplift provided companies with a tax deduction based on their investment costs, the production allowance offered a deduction based on the company’s revenues. This gave companies stronger financial incentives to cut costs where possible.

Additionally, companies were now allowed to start depreciation for the special tax in the same year the investments were made, rather than waiting until the field entered production. Under the new rules, companies could begin recovering the state’s share of costs the year after the investment was made. Under the old tax regime, companies had to wait until the field was in production.

The ability to start depreciation from the year of investment, rather than from production start, did not benefit Gullfaks—since the field was already in production and would begin depreciation regardless. Furthermore, Gullfaks was still subject to the production fee and was not covered by the new production allowance.